Following a period of keynesian-led relative redistribution in developed market economies, a mix of government action and corporate economic interests led to a radical reshuffling of capitalism. Two logics organize this reshuffling. One is systemic and gets wired into most countries’ economic and (de)regulatory policies—importantly, privatization and the lifting of tariffs. We can see this in the unsettling and de-bordering of existing arrangements within the deep structures of capitalist economies. This unsettling took place through the implementation of specific fiscal and monetary policies in most countries around the world, albeit with variable degrees of intensity. The effect was to open global ground for new or sharply expanded modes of profit extraction even in unlikely domains, such as subprime mortgages on modest residences, or through unlikely instruments, such as credit default swaps, a key component of the shadow banking system.

The second logic is the transformation of growing areas of the world into extreme zones for these new or sharply expanded modes of profit extraction. The most familiar instances are global cities and the spaces for outsourced work. While radically different types of sites, both have become thick local settings that contain the diverse conditions that global firms need—diverse labor markets, specific deregulations and contract guarantees, particular infrastructures and built environments. There are other such local settings for global capitalism, notably the vast purchases of land in Africa and Central Asia to grow food, to mine for rare metals, and to extract water.

A new kind of global economy formed, one centered on powerful firms using national governments to make private global space for their operations.[1] This contrasts with the international economy of the post–World War II era, which was centered on international trade and capital flows governed in large part by states, no matter their unequal power to do so. Both periods are marked by the concentration of power. But there was a sharp turn in the 1980s that marks a new, complex, but brutal phase of what we can actually call primitive accumulation; only now it is the very advanced sectors of the economy that are appropriating the resources of what was till recently the “advanced” capitalist economy. No sector illustrates this as well and as dramatically as high finance, the most complex and also the most predatory advanced sector. Finance has decimated the traditional, mostly local, bank.

The first section of this essay focuses on the capacity of finance to impose its logics across economic sectors. This financialization is a matter, not just of the volume of finance, but, more importantly, of its logic becoming wired into a growing number of economic sectors. Here I am particularly interested in examining the capacity of financial institutions to invent instruments that allow them to build high financial value from modest assets, often at a high cost for the owners of those modest assets. Next I focus on the irruption of the 2008 crisis and what it reveals about a system and its limitations—more a crisis of panic than a response to subprime mortgage losses and more a question of abuse by the top than by irresponsible consumers.

The Rise of Predatory Formations[2]

A key difference that marks the current period of advanced capitalism is the extreme power gained by particular types of private actors and the extensive participation of national governments in the making of this private global space. This participation is especially centered in the executive branch of government (whether presidential or prime ministerial). In my analysis, this branch of government has actually gained power through that participation. In this finding I go against much of the prevalent scholarship, which deals with the state as a whole and tends to see a zero-sum relation between “the” state and the global economy, along the lines of “what one gains, the other loses.”

Through the work of making private powers, the executive branch has also gained more private, unaccountable power, even as the legislative branch of government has become weaker.[3] This divergent trajectory is critical to my analysis. The legislatures/parliaments are the ones that have lost power in the current period: privatization and deregulation hollow out the functions, responsibilities, and powers of this branch. In fact, we have seen a transfer of some of these functions to private commissions set up inside the executive branch to handle the deregulations of finance, telecommunications, energy, and other key economic sectors. This is a much-neglected aspect of the current global era, since the dominant understanding sees “the” state as weakened by globalization. In fact, it is important to make internal distinctions: we are seeing a growing distance between the executive branch and the other branches, adding to the differential impacts of globalization on the state and to heterogeneity inside the state.

Critical to the particular process of economic globalization that took off in the 1980s was the need for the financial sector to count on the implementation of specific regulatory changes in order to enable the making of a global operational space, notably for finance. One of these rules was the privileging of inflation control over job growth—traditionally an unacceptable choice in electoral democracies. Having very diverse inflation levels across the world was extremely problematic for the growth of a global financial market.

A second change was the deregulation of interest rates, which had for decades been tightly controlled. This deregulation was a crisis for small banks and credit unions that depended on fixed interest payments for their survival; it is estimated that in the United States, where it all started, over ten thousand such entities closed over the ensuing two decades. Their losses were the gain of large banks. Thus, these large banks now account for up to 70 percent of consumer banking in the United States, charging consumers for every possible service and, above all, benefitting from a robust supply of consumers’ cash on which speculative financial instruments can be developed. Most consumer banking can be handled by small local banks and it should function through such local banks, also more likely to recirculate gains in the community.

A third adjustment concerned the need for financial firms to be able to invent extremely speculative financial and organizational instruments to engage in what are, ultimately, new forms of obtaining profit.[4] An ironic consequence of the growing complexity of finance was the implementation of systems geared toward financial forms of primitive accumulation. It took work, but advanced financial innovators and firms succeeded in articulating enormously complex financial and organizational instruments with elementary forms of extraction.[5] It is this latter issue that I develop in this article.

A case that illustrates this in a simpler way than does finance is the outsourcing of jobs. This widespread practice that accelerated in the 1980s is not only about lowering wages and (sometimes) avoiding environmental regulations. The insidious element is that millions of saved cents per hour of labor translate into a particular categorical positive: gains for shareholders as registered in the financial valuation of a firm in stock exchanges and other financial markets. The decreased cost can also contribute to increases in firms’ profit margins and consumers’ savings, but the invention of instruments to transform savings of labor costs into a more highly valued corporate outcome (i.e., valuation of a firm’s shares) was crucial to the strategy.

Creating Financial Value from Modest Assets

The financial sector has had a particularly creative phase since the 1980s with regard to the making of complicated financial instruments aimed at often simple extractions of profit from even very modest types of debt—student loans, used-car loans, mortgages for low-income households. Securitization was a key bit of financial engineering enabling such extractions and, more importantly, making them highly profitable. In the 1980s we see the beginnings of innovations enabling financial firms to bundle millions of small consumer debts and modest home mortgages in order to develop investment instruments for, and this is critical, the high-finance circuit.

One key example, and the one I will focus on to illustrate some of these issues, is that of the so-called subprime mortgage and the so-called subprime mortgage crisis. In early 2000, a type of subprime mortgage was developed in the United States that became catastrophic for modest-income households. Although subprime mortgages can be valuable instruments for such households, enabling them to buy a house or obtain a second mortgage or a mortgage on an already-paid-for home, what happened in the United States beginning in the mid-2000s was an abuse of the concept.

Presented with the possibility (which turned out to be mostly a deception) of owning a house by signing a contract with no payments for the first five years, many modest-income households were persuaded and signed. In signing the contract they enabled the development of an “asset”-backed security that could make profits for investors. By 2004 the strategy was so successful with investors that mortgage sellers did not even ask for a credit report or down payment, just a signature on the contract. In a financial world overwhelmed by speculative capital, all that mattered was the contract representing the material asset (the house). Indeed, subprime mortgage sellers were, we now know, indifferent to whether or not those households could make monthly payments. All that mattered was a contract that represented an actual asset. This low-grade asset (the very modest house) was to be mixed with high-grade debt so as to camouflage its low value.

Speed and numbers also mattered, so the goal was to sell subprime mortgages to as many households as possible as quickly as possible. We now know (and multiple lawsuits have been launched on this basis) that these particular types of mortgages were also pushed onto households that actually qualified for a regular mortgage, which would have afforded them more protections but would have taken much longer to process. For the “innovation” to work, sellers needed to secure five hundred or so contracts (mortgages) within a given time frame. Once mixed with high-grade debt (again, to obscure the low value of the asset), they were sold on the high-finance circuit as asset-backed securities. The negative effects on households, on neighborhoods, and on cities were given no consideration.

From the investors’ perspective, the key was the growing demand for asset-backed securities in a market where the outstanding value of derivatives was over US$600 trillion, more than ten times the value of global GDP. To address this demand, even subprime mortgage debt could be used as an asset. But the low quality of this debt necessitated cutting each mortgage into multiple tiny slices and mixing them with high-grade debt. The result was an enormously complex and opaque instrument. This opacity is well illustrated by now-defunct Lehman Brothers, whose value still has not been fully established by a team of top-level experts who have been working for years on the company’s bankruptcy proceedings.

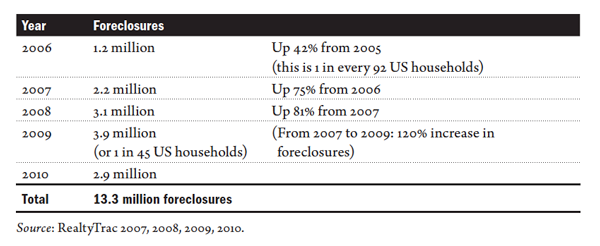

The lethal threat to these households was that their capacity to pay the monthly mortgages mattered less, if at all, to the sellers of those mortgages than did the securing of a certain number of loans, within a short time span, to be bundled up into “investment products.” The use of complex sequences of operations delinked the creditworthiness of the home buyer from investors’ profit. Also, the accelerated buying and selling of these instruments in the high-finance circuit enabled profit making while passing on the risk to the next buyer. Investors made hundreds of billions of dollars in profits on these problematic asset-backed securities. At the same time, millions of those modest households have and continue to go bankrupt and lose their homes and whatever savings they had put into them, while many investors made vast profits. Table 1 shows the short and brutal history of the rapid growth in the number of foreclosures. Of the 13.3 million foreclosures, 9.3 million ended in evictions, probably affecting over 30 million individuals.

Table 1 U.S. Home Foreclosures, 2006–2010

The insidious element of these transactions, as with the outsourcing of labor, is that a very large number of mortgages sold to modest-income households (which mostly did not ask for these mortgages) can actually translate into a categorical positive (profits) for the high-finance investor. It took serious financial engineering to make this possible, just as it did to increase corporate shareholder value through outsourcing jobs. The millions of bankruptcies among subprime mortgage holders in 2006 and 2007 did not affect investors directly: only those firms that held on to these mortgages suffered. Most investors did not hold on and thus made profits. But within the logic of finance, it is also possible to make a good profit by betting against the success of an innovation, predicting failure.[6] And that type of profit making also happened.

In short, the so-called subprime crisis was not due to irresponsible households taking on mortgages they could not afford, as is still commonly asserted in the United States and in the rest of the world. Households were mostly used by banks and agents, who created a foreclosure crisis for homeowners. The estimate by the Federal Reserve Bank is that 15 million subprime mortgage contracts were signed over a period of less than ten years. Indeed, the Federal Reserve Bank estimates that total foreclosures will reach close to 14 million by 2014.

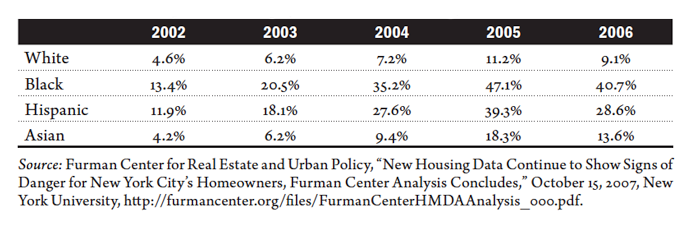

Whole neighborhoods were devastated and municipal budgets destroyed. New York City illustrates some of the specifics: table 2 shows how white residents, who mostly have higher average incomes than all the other groups in the city, were far less likely to wind up with subprime mortgages than all other groups, reaching just 9.1 percent of all mortgages taken by whites in 2006—a high point—compared with 13.6 percent of Asian Americans, 28.6 percent of Hispanic Americans, and 40.7 percent of African Americans. The table also shows that all groups, regardless of incidence, had high growth rates in subprime borrowing from 2002 to 2006. If we consider the most acute period, 2002–5, the rate more than doubled for whites, tripled for Asians and Hispanics, and quadrupled for blacks.

Table 2 Rates of Subprime Lending by Race in New York City, 2002–2006

Blowback: A Crisis of Confidence

But the game of mirrors that is part of highly speculative finance did suffer a setback. The millions of foreclosures generated a crisis of confidence in the larger financial system: in 2008, the year that the larger financial crisis exploded, an average of 10,000 US households lost their homes to foreclosure every day. The sharp rise in foreclosures over a very short period of time signaled that something was wrong. But, in an ironic blowback, the mixing of subprime mortgages with high-grade debt made it almost impossible to trace the toxic component in the financial system’s investments. And this is what generated a crisis of confidence that brought the vast financial system to its knees, at least temporarily. It was the little tail of trust that wagged the huge body of finance.

This brief and brutal experiment was a form of primitive accumulation achieved through an enormously complex sequence of instruments using vast talent pools in finance, law, accounting, and mathematics in order to make modest assets work for the high-finance circuit, without any regard to the equally modest holders of these assets. It illustrates how financial institutions can “make” major additions to financial value on very modest assets and, most importantly, can do so with a full disregard for social outcomes and even for the “national economy.” This disregard is legal, no matter its actively destructive effects on households, neighborhoods, and municipal governments.

Finally, we should remember that the complexity of the meaning of “gains” in finance contrasts with traditional banking gains. In traditional banking the gains are on the sale of money the bank has, while in finance the gains are on the sale of money the institution does not have. As a result, finance needs to “make” capital, and this means the creation of speculative instruments and the financialization of nonfinancial sectors, subjects I develop more fully elsewhere.[7]

Conclusion: Finance Is Not About Money

Financial profit is a construction that either can be promptly materialized in a nonfinancial asset, such as an investment in building a dam or buying a telecommunications corporation or developing public housing, to mention just some materializations, or can be used as a platform for further financial constructions (i.e., speculation). The latter, partly facilitated by the use of electronic networks, “softwared” financial instruments, and the invention of many new derivative-based instruments, has been dominant in the last twenty years. It has generated the extremely high levels of financialization now evident in several major developed countries.

More generally, and to give a sense of the orders of magnitude that the financial system has created over the last two decades, the total (notional) value of outstanding derivatives, which are a form of complex debt and the most common financial instrument, reached a quadrillion US dollars in 2013. This is mostly money that does not exist. And this is what leads me to argue that finance is not about money: it is a capability. How we use it does matter.

Saskia Sassen is the Robert S. Lynd Professor of Sociology and Cochair of the Committee on Global Thought, Columbia University (www.saskiasassen.com). Her new book is Expulsions: Brutality and Complexity in the Global Economy (Harvard University Press/Belknap, 2014). Older books include the fourth, fully updated edition of Cities in a World Economy (Sage, 2012), Territory, Authority, Rights: From Medieval to Global Assemblages (Princeton University Press, 2008), A Sociology of Globalization (W. W. Norton, 2007), and The Global City (Princeton University Press, 1991/2001). Her books have been translated into over twenty languages. She has received diverse awards, including multiple doctorates honoris causa and the 2013 Principe de Asturias Prize for the Social Sciences, and has been chosen as one of the Top 100 Global Thinkers by Foreign Policy (2011), one of the Top 100 Thought Leaders by GDI-MIT (2012 and 2013), and one of the Top 50 Global Thinkers by Prospect Magazine (2014).

-

Saskia Sassen, Territory, Authority, Rights: From Medieval to Global Assemblages, rev. 2nd ed. (Princeton, NJ: Princeton University Press, 2008), chaps. 4–5. ↩

-

I develop this concept of predatory formations in Expulsions: Brutality and Complexity in the Global Economy (Cambridge, MA: Harvard University Press/ Belknap, 2014). Very briefly, these are assemblages of technical capacities and networks, legal and accounting instruments, and owners or managers of capital. My key intention is to capture something that goes well beyond the mere fact of concentration of wealth in the hands of very rich people. The existence of predatory formations makes the current phase so difficult to bring under control. ↩

-

Sassen, Territory, Authority, Rights, chap. 4. ↩

-

I develop this proposition in “Mortgage Capital and Its Particularities: A New Frontier for Global Finance,” Journal of International Affairs 62, no. 1 (2008): 187–212. ↩

-

This is only one component of the financial system. There are many components of finance that consist of interactions among rich and powerful investors where these particular mechanisms of primitive accumulation may not be an issue. And there are some other major components that also are subject to mechanisms of primitive accumulation, notably pension funds and mutual funds, which often have to pay multiple little fees and commissions that amount to significant and unwarranted losses for the pensioners and the consumers who buy shares in mutual funds. ↩

-

They speculated against these instruments. That is to say, they betted against the sustainability of instruments that were based on getting low-income people to sign off on mortgage contracts regardless of their capacity to pay. This strongly suggests that many of the damaging aspects of these instruments for the households were known in the financial community. ↩

-

Sassen, Expulsions, chap. 3. ↩